Is Inflation Good or Bad for the Economy?

The Federal Reserve (Fed) typically targets an annual rate of inflation for the U.S., which at present is 2 percent. Although high inflation can hurt an economy, deflation, or falling prices, is not desirable either. The belief is that slowly increasing price levels keeps businesses profitable and prevents consumers from waiting for lower prices before making purchases. When prices are falling, however, consumers delay making purchases, if they can, anticipating lower prices in the future. For the economy, this means less activity, less income generated by producers, and lower economic growth. Others argue that inflation is less important and even a net drag on the economy. Rising prices make savings harder, driving individuals to engage in riskier investment strategies to increase or even maintain their wealth.

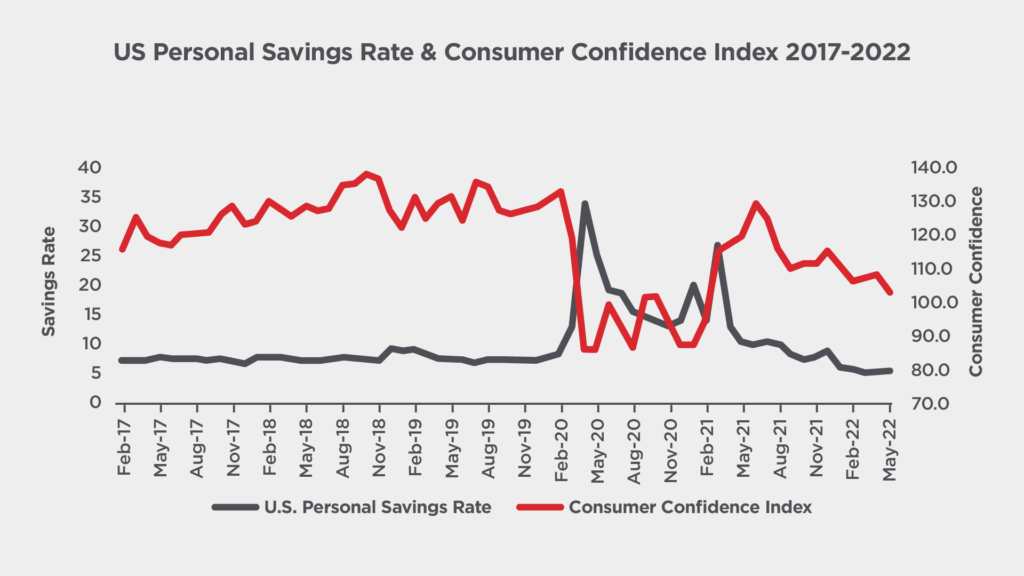

In the current climate, a persistently high inflation rate will continue to weigh on income, albeit to a diminishing extent as inflation is expected to stabilize by the end of 2022. Currently, trends show that households have reduced their saving rates to manage the rising cost of living. Those rates are now back to pre-pandemic levels, which indicate that there is limited scope for them to fall further. With consumer confidence falling to even lower levels in May 2022, it seems that spending growth is projected to weaken in the second quarter of 2022. This will have the effect of stifling U.S. Gross Domestic Product (GDP) growth since consumption is the main driver of economic growth in that economy.

Source: Bloomberg

Inflation Dynamics

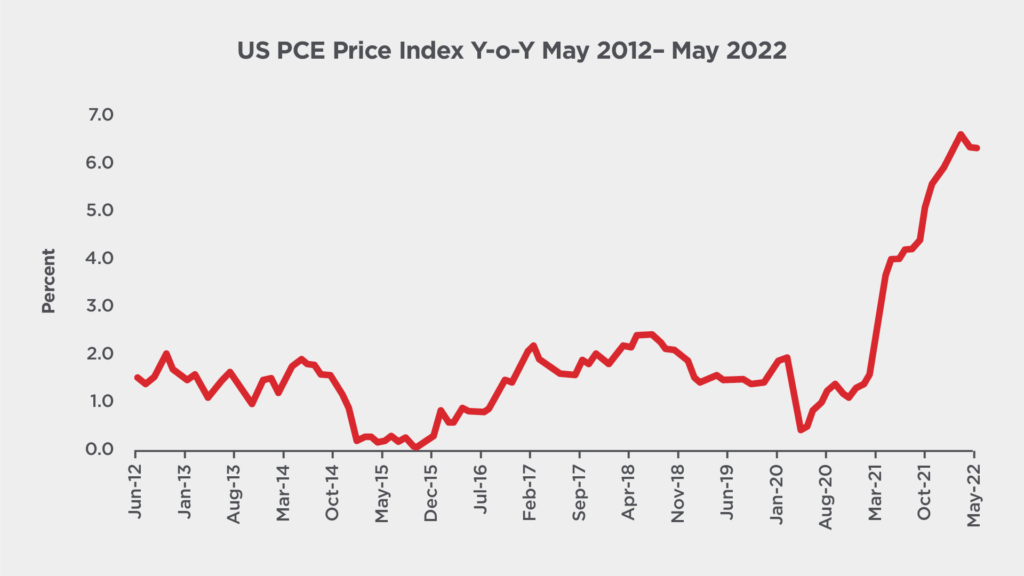

The Fed’s preferred gauge of inflation is the price index for Personal Consumption Expenditures (PCE). The PCE, which is released monthly, reflects the measure of changes in the price of goods and services purchased by the average U.S. consumer. After more than a decade of sub 2 percent inflation, PCE has risen rapidly from a low of 0.4 percent in April 2020 to 6.3 percent in the most recent May 2022 data.

Source: Bloomberg

Robust acceleration in services spending into the end of the first quarter of 2022 suggests that the rotation from goods to services is ongoing, as the U.S. consumer increasingly pays for experiences as opposed to household goods as the impact of the pandemic recedes. However, many businesses struggled to keep up with demand, particularly as they faced Covid-related disruptions in production and supply chains. These factors first showed up inflation data in early 2021 as activity began to normalize. Prices rose sharply for goods that were especially sensitive to supply chain problems and for services that were just beginning to reopen from the pandemic shutdowns. Motor vehicles were a prime example of this occurrence. In the early stages of the pandemic, the demand for cars plummeted and their prices declined. However, with high demand for personal as opposed to public transport and low borrowing costs, vehicle demand quickly turned around. Automakers were unprepared for the surge, expecting a severe and prolonged recession, they had substantially scaled back their production plans and ordered fewer of the microprocessors that are present in most vehicles today.

How Policymakers Manage Inflation?

The Federal Reserve is tightening monetary policy to fight inflation. More precisely, it is raising the short-term interest rate, known as the federal funds rate. This is the interest rate that commercial banks use to make overnight loans to other banks. Increasing this rate will increase the cost of borrowing for banks that need funds. Banks naturally pass on these higher costs of borrowing to consumers and businesses. This means that if the Fed raises its federal funds rate by 75 basis points, or 0.75 percentage points as it did in June, consumers and businesses will also have to pay more to borrow money. How much more depends on many factors, including the maturity of the loan and how much profit the bank wants to make. A higher cost of borrowing means that access to money becomes more expensive. The higher cost of borrowing will dampen general demand and economic activity. For example, if the interest paid on a car loan increases, the consumer if be less inclined to borrow money at this time to purchase a car. In terms of businesses, decisions to borrow will be hampered by a rising interest rate, so capital expenditure on new infrastructure may be delayed. This impact on demand, by increasing interest rates, has the effect of lowering inflation. Even small increases in interest rates can have ripple effects that significantly slow down economic activity, limiting the ability of companies to raise prices.

History of Fed Funds Rate and Economic Growth

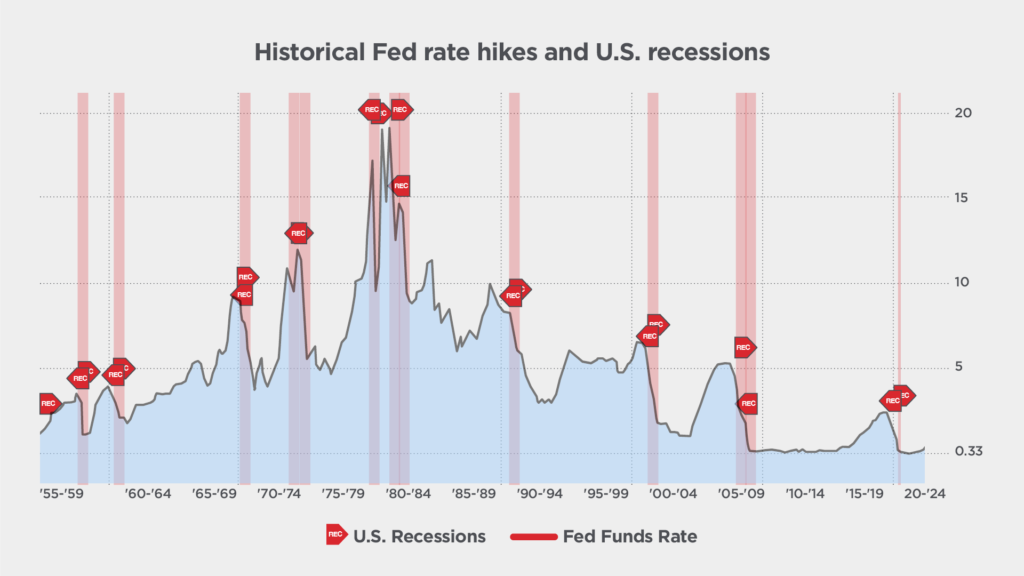

Higher interest rates have the impact of driving down inflation by making debt more expensive. For this same reason, increasing interest rates can also trigger an economic downturn. In fact, for the last eleven instances since 1955 when the Fed raised rates to counter inflation, recessions followed all but one time. The only exception was in 1994, which was a situation where the Fed avoided the situation of pushing the economy into a recession. The Federal Reserve chair, Jerome Powell, has said that he is aiming to engineer a “soft landing”, which is a gradual slowing of economic activity that helps curb rising prices without jeopardizing the recovery. However, this remains a challenge as the drivers of economic growth are in a delicate situation. The U.S. economic outlook will also have external factors that are beyond the control of the Fed to contend with, namely the impact of the conflict between Russia and Ukraine.

Source: Bloomberg

Inflation in a Local Setting

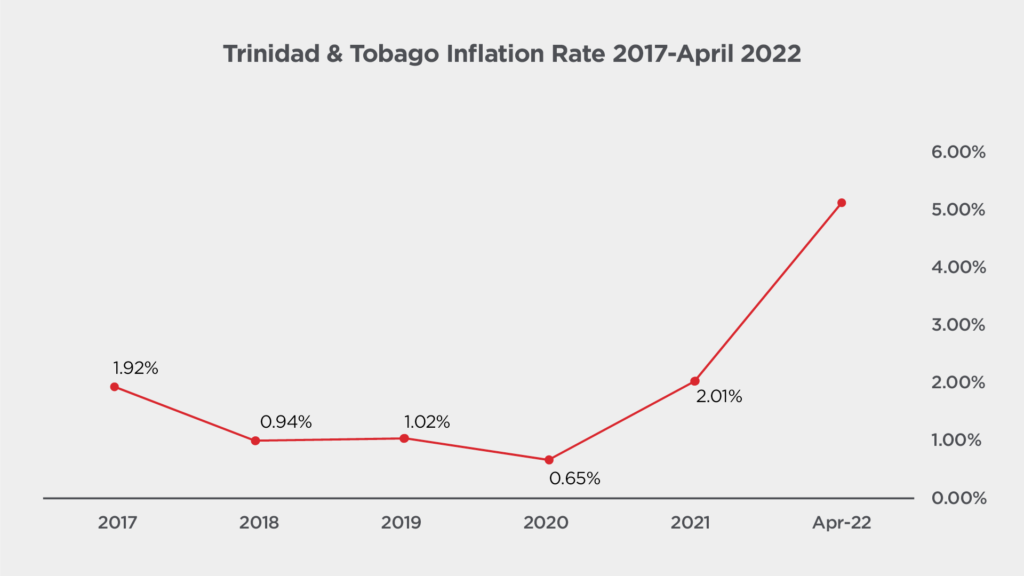

Like the global economy, domestic prices have been rising. The latest data from the Central Statistical Office (CSO) suggest that the year-on-year inflation rate have risen to 5.1 percent as at April 2022. It is expected that imported inflation, which is the general price increase due to an increase in the costs of imported products or services, will continue to push up local prices of food products and other items in the coming months.

Taking these factors into consideration, the Central Bank of Trinidad Tobago (CBTT) has agreed to maintain the repo rate at 3.5 percent. The repo rate is the rate at which the central bank lends money to commercial banks in the event of any shortfall of funds. The repo rate is used by monetary authorities to control inflation by influencing the lending rate used by commercial banks. Commercial banks can choose to pass on this increase in the rate of borrowing from the central bank to the customer. A higher cost of borrowing normally limits the access to cheaper money to the customer. A reduced access to cheaper money through borrowing in turn will have the effect of lower demand for goods and services, which should lead to a decline in inflation, from a demand perspective.

Due to the eroding effect of inflation on the value of money, individuals and institutions alike are encouraged to invest to preserve the value of their assets. Many investments have been historically viewed as protection against inflation. For instance, if the average annual inflation rate is expected to be 2 percent, to keep up with inflation an investor would need to build a portfolio with the potential to return at least 2 percent to maintain their purchasing power. Instead of holding onto excess cash, one can invest it in company stocks or a mutual fund. This is a prudent way to protect one’s assets against rising inflation. Additionally, investment returns can help maintain a specific standard of living, during a time of rising expenses.