Asset allocation is an investment strategy that involves spreading your funds across various asset classes such as stocks, bonds, cash and cash equivalents. The importance of dividing your money in various asset classes is to reduce investment risk. Investment risk is reduced by investing in assets that do not have the same risk and return characteristics, meaning they do not respond in the same way to the same market forces at the same time. Ideally, if one particular asset class is underperforming or incurring losses, another asset class should be posting gains, thus netting off or reducing the size of the losses.

As mentioned before, the three primary asset classes are stocks, bonds and cash and within each asset class are subcategories. Some subcategories include:

- Stocks – Domestic equity, International equity, Emerging market equity, Large capitalization stocks, Mid-capitalization stocks, Small capitalization stocks .

- Bonds – Corporate debt, Government debt, Domestic bonds, International bonds, Emerging market debt.

- Cash and cash equivalents– Savings accounts, Treasury bills, Mutual funds (money market and income funds)

Deciding on what asset allocation is best for you is one of the most significant investment decisions you can make as it will impact your overall portfolio return and will determine if you will meet your financial goals. If you opt not to have a portion of your investment portfolio in risky assets such as stocks, you are at risk of not generating the level of return that is required to meet your long term goals. In cases of rapidly rising prices, stocks act as an inflation hedge, thus if you are underweight stocks, that is if you have less stocks, there is a possibility that your portfolio’s purchasing power will be eroded.

On the other hand, if you have a short term goal and you have too much stocks in your portfolio, when the prices of your stocks decline, you can suffer significant losses and there lies a risk that your entire portfolio maybe wiped out.If you need help with this process it is strongly recommended that you secure the services of a Financial Advisor who can provide professional expertise in this area that is specific to your goals and objectives in your portfolio.

How to get Started

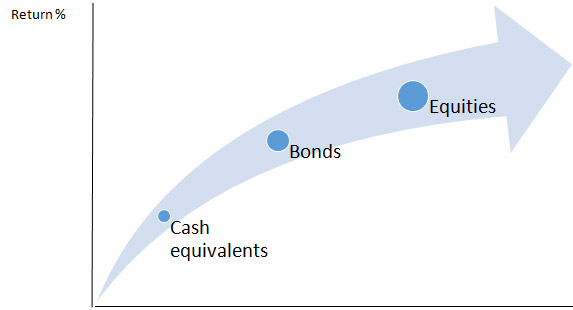

The first step to determining your asset allocation mix is to gain an understanding of the risk-return characteristics of the various asset classes. Figure 1 compares the risk and potential return of some popular choices

Figure 1: Risk-return characteristics

Stocksare very volatile and have the highest potential return, but they also have the highest risk. Cash equivalents that includes Treasury bills / Government Treasuries have the lowest risk since they are backed by the government, but they also provide the lowest potential return.

Investors who have the ability and disposition to tolerate fluctuations in value will be more inclined to invest in stocks. In contrast, investors with a low tolerance for wide swings in value will prefer bonds and money market securities.

An investor’s risk tolerance is determined by the following four (4) factors:

- Age – the younger you are, the greater the ability to tolerate risk as you would have enough time to recover from any losses that you may incur. Generally, a person’s ability to accept risk should begin at a high level and gradually decline over their lifetime.

- Time horizon – this refers to the time frame within which your goals must be met. Thus, the shorter the time period to achieve your goals, the lower tolerance you would have to withstand wide fluctuations in your portfolio.

- How critical are your goals – the importance of your goals and the subsequent consequences if they are not met influences the degree of risk that can be assumed. Thus, if you are depending on your investment portfolio to meet daily expenses and to live, there is a very low tolerance for volatile investments.

- Willingness to take risk – if you have personal experience with significant losses and gains, you would be in a position to understand the risk involved and be mentally prepared for the associated dips in your portfolio.

Table 1 below illustrates the general rule of thumb:

Table 1: Risk Tolerance

The next step is for you to be aware of any constraints you may have and includes the following:

- Liquidity needs – if you are dependent on your investment portfolio to meet daily living expenses, there is a need for the assets that will be selected to have a certain degree of liquidity. Assets such as money market instruments and Treasury Bills may suit your investment needs as such assets can be sold fairly quickly without a significant loss in its price. Investments in venture capital funds or real estate may not be suited for your needs.

- Taxes – taxes are normally levied on income, gains and on assets that are transferred from one owner to another. The various tax rates should be compared and the asset that carries the least tax burden should be selected – once it is aligned with your return objective and risk tolerance. For example, if the income tax rate is higher than the capital gains tax rate, it will be beneficial for you to have a greater proportion of your assets in equities than fixed income securities to benefit from the lower capital tax rate.

- Unique circumstances – as an investor, you may have a personal stance against investing in certain companies located in particular industries such as tobacco and alcohol.

Knowing your risk tolerance and your constraints that puts you in a better position to create your own asset allocation. The higher tolerance of risk and the fewer constraints you have, the more volatile securities you can include in your portfolio and the greater the return.

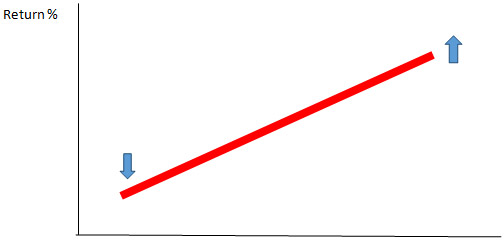

Please bear in mind – the riskier the assets, the higher the return you can achieve and this is referred to as the risk-return tradeoff (see Figure 2). While you may select more volatile assets, because your portfolio is invested in other asset classes, there is some degree of protection. Since different assets have different risks and market fluctuations, proper asset allocation protects your entire portfolio from the ups and downs of one single class of securities.

Figure 2: Risk / Return Tradeoff

Given the varying risk appetites of investors, investment companies normally have a series of model portfolios with different risk and return profiles. Such portfolios comprise the various asset classes in varying proportions and satisfies investors’ different risk tolerances.

Model portfolios normally range from conservative to aggressive as illustrated in Figure 3.

Figure 3: Model Portfolios

Conservative Portfolios are tailored to investors with a low risk tolerance and generally has a large percentage of the portfolio in lower risk securities such as fixed-income and money market securities. Such securities don’t fluctuate widely in value and thus aids in preserving the investor’s capital or principal value.

On the other end of the spectrum is the Very Aggressive portfolio that consists mostly of equities. There is the risk that the portfolio’s value will vary widely in the short term, but the return potential is also very high over the long term and the portfolio is thus positioned for capital growth.

How you allocate your money among major investments and asset classes greatly influences your returns. Stocks and other types of ownership investments are riskier and more volatile, thus you must have a long-term perspective when investing in such assets. Treasury bills, bonds and mutual funds are not as risky and are more suitable when you are investing over the short term. Selecting good investments involves matching the time frame and your ability to tolerate risk to the riskiness of the investment.

We at the UTC Advisory Services Department are readily available to help you with any financial matter as it pertains to getting closer to your financial goals. Our Financial Advisors are equipped with the knowledge and experience to guide you in the asset allocation process that will enable you to have a portfolio with the right mix of assets that will meet your return objectives and your risk tolerance.

MF 4TH JUNE 2014

You should consult with a Financial Advisor at the UTC, who can assist you in planning major life decisions and events.