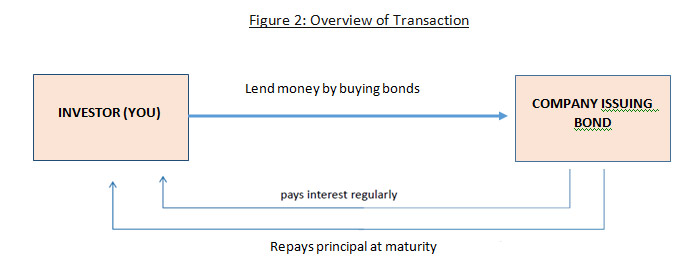

A bond is similar to a loan that the buyer, or bondholder, makes to the bond issuer. Bonds are issued by companies and government bodies to fund their day-to-day operations or to finance specific projects. When an investor buys a bond, he or she is, in fact, loaning money for a certain period of time to the issuer of the bond. In return for loaning funds, investors receive the principal amount back, with interest, at the time the bond comes due or “matures”.

In the bond market, certain terms are used to describe the bonds:

- Face value / Par value– this is the amount paid to a bondholder at the maturity date.

- Coupon – amount of interest which a bond issuer pays to a bondholder at each payment date.

- Maturity date – the date on which the issuer has to repay the face.

For example, you decide to purchase a bond with a face value of $1,000, a semi-annual coupon of 8%, and a maturity of 10 years. What does this mean?

It means that:

- You’ll receive two interest payments of $40 every six months for 10 years.

- When the bond matures in 10 years, you’ll get your $1,000 back

How do you calculate how much you will receive every six months? The following formula is normally used:

The coupon payment on each of this bond $40 = $1,000*(8%/2).

This means that you will receive $40 every six months.

How bonds are different when compared to equities?

Bonds are very different to equities. While as a purchaser of a stock, you become an owner in a corporation and are entitled to voting rights and a share of the company’s future profits. As a bond investor however, you become a creditor of the institution and are not entitled to the company’s future profits.

While you do not become part owner of a company when you purchase their bonds, as a bond holder, you have higher claims on their assets than shareholders. Thus in the case of bankruptcy, you will receive your invested funds before the shareholders.

As markets become volatile, many investors turn to bonds as an alternative to stocks as bonds are often deemed as “safe” investments. While bonds can play an integral role in a well-diversified portfolio, investors should fully understand their characteristics and inherent risks? before investing.

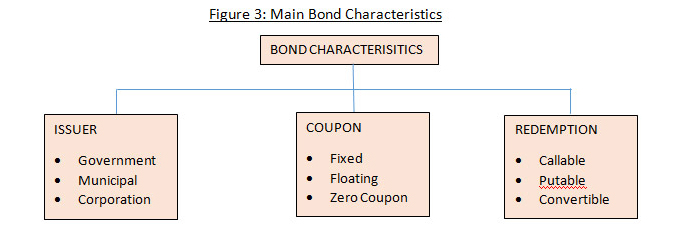

Bond Characteristics

Issuer

Government bonds– these are bonds issued by sovereigns or governments. Such bonds are backed by the full faith and credit of the particular government and are considered low risk as it is unlikely that the government will not repay its debt.

Municipal Bonds – Municipal bonds are bonds issued by states, cities, towns, or public commissions to provide money for schools, hospitals, and other public works. This type of bond is not issued in the local capital market.

Corporate Bonds – such bonds are issued by corporations in the need of capital. Corporate bonds, unlike government bonds may carry greater risk, thus it is critical that investors understand the quality of the bond they are considering to buy.

Coupon

Fixed Rate Bonds – these bonds pay an absolute coupon rate over a specified period of time. Upon maturity, the last coupon payment is made along with the par value/ face value of the bond.

Floating Rate Bonds – such debt instruments pay a coupon rate that varies according to market conditions and is normally linked to an underlying benchmark (the interest rate that is linked to the bond) such as the three, six or nine-month T-bill rate or LIBOR.

Zero coupon– these bonds are also known as accrual bonds do not pay a coupon. Instead, these types of bonds are issued at a deep discount and pay the full face value at maturity.

Redemption

For fixed rate bonds, both investors and issuers are locked into either receiving or paying a set coupon rate over a specified period of time. Given the tenure of the bond, there is a great likelihood that interest rates can move either above or below this fixed coupon rate. For this reason, some bonds offer additional benefits to investors or more flexibility for issuers:

- Callable, or a redeemable bond features gives a bond issuer the right, but not the obligation, to redeem his issue of bonds before the bond’s maturity. Since the bond is being redeemed before its maturity date, the issuer, must pay the bondholders a premium.

In a declining interest rate environment, this option is ideal for the Issuer as they can call their bonds and refinance their debt at the lower interest rate. - Putable bonds give bondholders the right but not the obligation to sell their bonds back to the issuer at a predetermined price and date. This option benefits the investor especially in a rising interest rate environment. Rather than being stuck with a bond that is paying a lower coupon, the investor can sell – their bonds back to the issuer and reinvest their money at a higher interest rate.

- Convertible bonds give bondholders the right but not the obligation to convert their bonds into a predetermined number of shares at predetermined dates prior to the bond’s maturity. Of course, this only applies to corporate bonds.

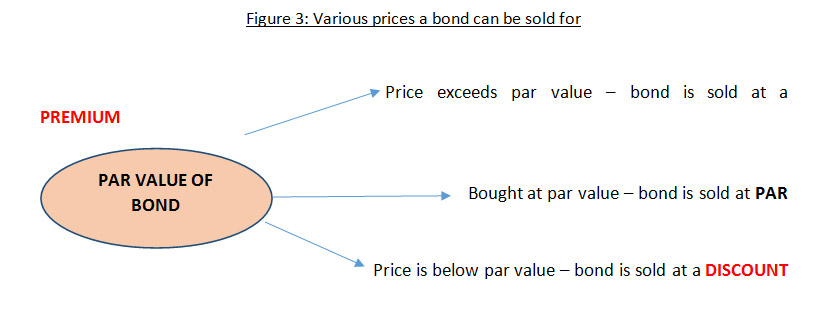

Bond prices and the level of interest rates

Just like stocks, the price of bonds will fluctuate throughout the trading dayand its lifetime/holding period.

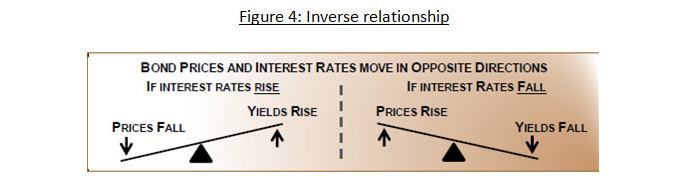

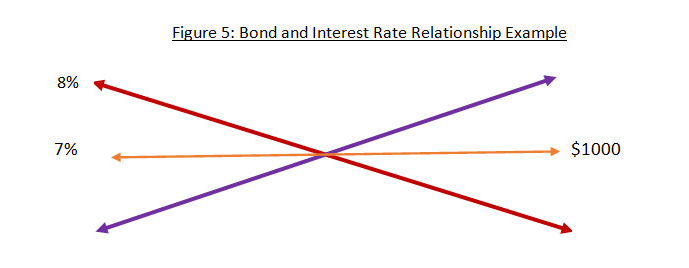

Bond prices fluctuates with changes in interest rates. Interest rates and bond prices have what is called an “inverse relationship” – meaning, when one goes up, the other goes down and is depicted in the graphic below.

For example, suppose XYZ companyoffers a new issue of bonds carrying a 7% coupon, meaning it would pay you $70 a year in interest. After looking at investment alternatives, you decide to purchase a bond at its par value, $1,000. After a year, interest rates in general go up and Figure 5 illustrates the associated price with the movement in interest rates.

Rationale

You initially bought the bond at a face value of $1000 and a coupon of 7%. Newly issued bonds are costing $1,000 and are paying an 8% coupon ($80 a year in interest). If you want to sell the bond, buyers will be reluctant to pay you face value ($1,000) for your 7% XYZ bond. In order to sell and peak investors interest, you would have to offer your bond at a lower price – a discount – that would enable it to generate approximately 8% to the new owner. In this case, that would mean a price of about $875.

Similarly, if rates falls below your original coupon rate of 7%, your bond would be worth more than $1,000. It would be priced at a premium, since it would be carrying a higher interest rate than what was currently available on the market.

RISKS

If you hold the bond to maturity and it is a coupon paying security, you will receive this fixed coupon payment for the length of the security’s tenure. While this payment is fixed, there are inherent risks associated with investing in bonds and they include:

- Interest Rate Risk: Due to the fact that bond prices move in the opposite direction of interest rates, there is the risk that price of outstanding bonds will fall. All bonds, including those issued by the governments are subjected to interest rate risk.

- Inflation Risk: Given that most bonds pay a fixed rate of interest, their value can be eroded by inflation as price increases reduces the purchasing power associated with the fixed income.

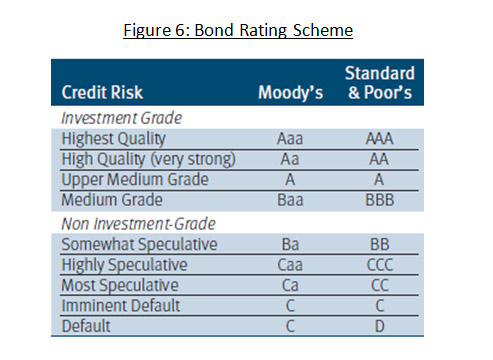

- Credit Risk: The risk that a bond issuer fails to make principal or interest payments when due to the fund or that the credit quality of the issuer declines.

To assess the credit quality of a bond, investors can look to organizations that rate various corporate bonds, such as Moody’s Investors Service and Standard & Poor’s. The bonds are normally categorized as Investment Grade (bonds that have a rating Baa or above by Moody’s and BBB or above by Standard & Poor’s) or Non-Investment Grade (also known as Speculative / Junk and has grades below investment grade).

If you need further clarification on the workings of the bond market you can seek the help and guidance of a Financial Advisor for any questions you may have.

You should consult with a Financial Advisor at the UTC, who can assist you in planning major life decisions and events.