Some of you may be wondering – what is the Business Cycle and what is its relation to stocks? The Business cycle is essentially the many phases that an economy goes through over a period of time. The phases are characterized by the level or intensity of economic activity and is gauged by critical economic indicators including Gross Domestic Product (GDP), the unemployment rate, the inflation rate and the level of interest rates, just to name a few. The length of each cycle varies and can last from a few months to a few years.

The performance of the economy tends to have a significant influence on the performance of financial markets. Aligned with the top down approach, companies do not operate in isolation. They operate and function within theirparticular industry, and in turn the industry functions within an economy. More often than not, whatever happens in the economy have a tendency to trickle down into the industry and in turn to companies.

The business cycle generally has four stages:

- Expansion

- Peak

- Contraction

- Recovery

In the Expansion stage, economic activity is rising and is marked by an expanding Gross Domestic Product (GDP), rising employment and strong credit growth. Due to the existence of spare capacity, inflationary pressures are low that aids in boosting corporate earnings and profits.

In the Peak stage, while the economy is operating at full steam, the pace of economic expansion is slowing down. GDP growth will still be positive, however, the rate of expansion will begin to decelerate. The output gap has narrowed considerably, employment is at near maximum levels and income levels start to rise. As a result of the closing in of the output gap and maximum employment, there may be evidence of inflationary pressures.

The next stage is Contraction and occurs when economic activity begins to decline and is characterized by a reduction in GDP, a rise in the unemployment rate, tightening of credit availability and a deterioration in corporate profits.

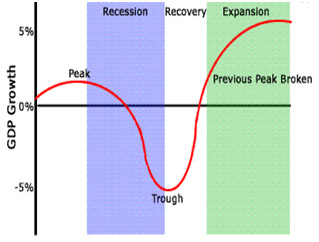

The Early recovery stage features a trough – this is where the contraction bottoms out and economic activity begins to pick back up slowly. Figure 1 provides a graphical representation of these four phases.

Figure 1: Phases of the Business Cycle

Stocks and other economically sensitive assets generally post the strongest returns during the early phase of the business cycle. As you may already know, when you purchase shares of stock, you become a partial owner of that particular company. As an investor, you are buying an asset – in this case a share of stock, with the hope that you receive a return. For shares of stock, the return comprises both dividend payments and an appreciation in the share price.

When an economy is in the early phase of its recovery and economic activity is growing, more often than not, company’s earnings and profits are also increasing. Against the backdrop of rising employment, which in turn will positively impact consumer demand, corporations will enjoy rising sales and revenues. With a low inflation rate owing to existing spare capacity, rising input prices and wage pressures do not pose a problem for many companies. With rising revenues and contained cost, companies’ earnings should rise and even exceed its quarterly earnings estimate. As companies report their better than expected results, more and more investors will want to own shares of those companies. On the stock market, such increased demand for a company’s share will create upward pressure on its price.

In addition, as profits climb, the company can create value for their shareholders by paying dividends, reinvesting the additional profits back into the company by expansion or research and development and even buy back their shares. Dividends are a major source of return for a shareholder, thus if companies are increasing their dividend payouts, more people will be attracted to the stock in order to benefit from the higher income.

Reinvesting the earnings and profits back into the company also secures one’s future. Investing in better technology, research and development and new products can greatly enhance a company’s future competitive advantage.

The same can be said if the economy is facing slowing growth. In the event that an economy is going through the peak and eventually contraction stage, the stock market would not perform as well as it did in the early recovery phase. Companies will be faced with slowing demand for its products, rising inflationary pressures as the output gap has narrowed and in turn rising operating cost. With a reduction in its revenue stream and higher operating cost structure, companies will fail to meet its earnings estimate and may see the price of their shares fall as investors loses confidence and rush to sell.

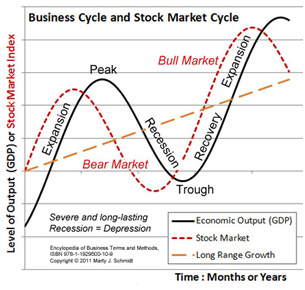

Figure 2: Business cycle and Stock Market Cycle

Based on the illustration in Figure 2, when the economy is going through its recovery and expansion stages of the business cycle, the stock market is experiencing a bull market. A bull market is essentially a rising stock market and is marked by strong investor confidence. The stock market is rising against the backdrop of a strong economy, low unemployment, high levels of consumer spending and increased business profits. As noted earlier, when businesses profit and earnings estimate beat its forecast, investors desire to get in on the action and they seek to buy stocks and hang on tight for the ride. The demand for shares outstrips its supply of shares as no one wants to give up their shareholdings. The competition to acquire those much-coveted shares becomes fierce, which drives the prices up even higher. Investors risk appetite is more aggressive and are willing to take on more risks due to the thriving economic environment.

In contrast, during the stages of trough and recession, the stock market is in a bear market. A bear market is a declining market and is characterized by a sharp drop in stock prices across the board. In a bear market, the economy tends to be weak – unemployment increases, consumer spending declines as a result, which in turn lowers corporate profits. Investors are not so eager to assume risk in a bear market as they are not as confident about their chances.

To conclude, stock values are driven by corporate earnings, and the business cycle is the primary impetus of changes in such earnings. While it is invaluable to be able to predict the turning points of the business cycle, actually doing so is very challenging as economists worldwide have yet to accurately predict such turning points with precision. More often than not, turning points are rarely identified until months later after the peak or trough has been reached.

You should consult with a Financial Advisor at the UTC, who can assist you in planning major life decisions and events.