One of the main assumptions that have pervaded the investment field is one of rationality. Investors are assumed to be rational beings and thus act rationally. A rational investor is one that considers all the available information that is out there before making a decision, thus decisions are always prudent and logical. This decision is assumed to lead the investor to a choice that will allow him / her the maximum benefit.

Figure 1: Rational Investor

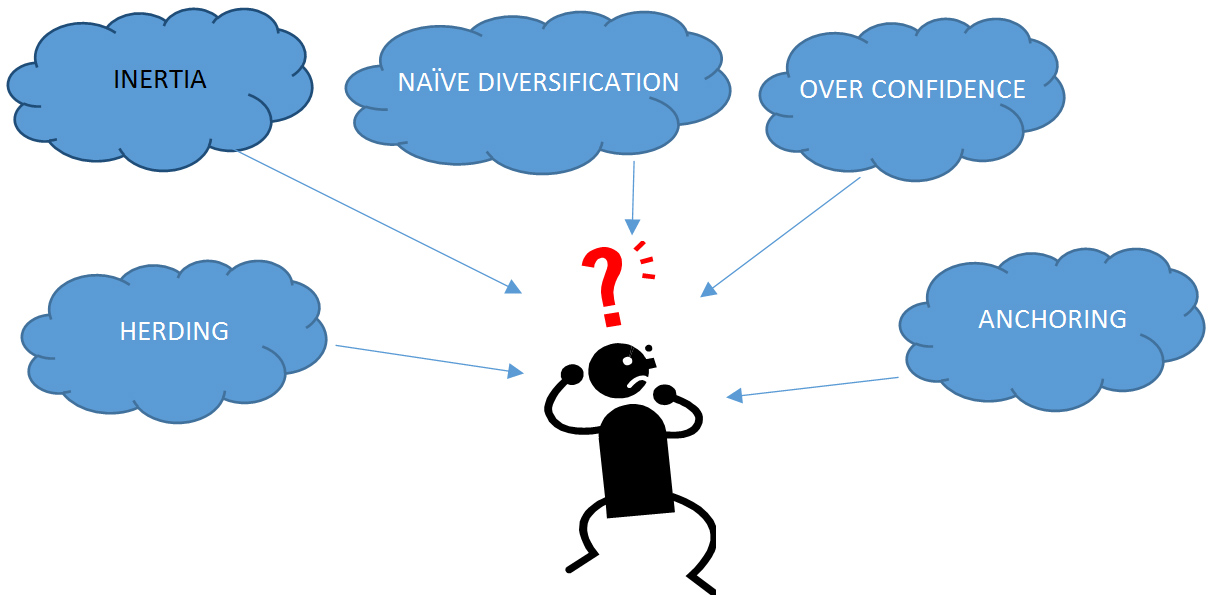

Often than not, this is not the reality for many persons. A person’s background, past experience and attitude can play a major role in their decision making process. As an investor it is important to be aware of any behavioral traits that you may exhibit and how it can affect the way in which you invest your funds.

Figure 2: Irrational Investor

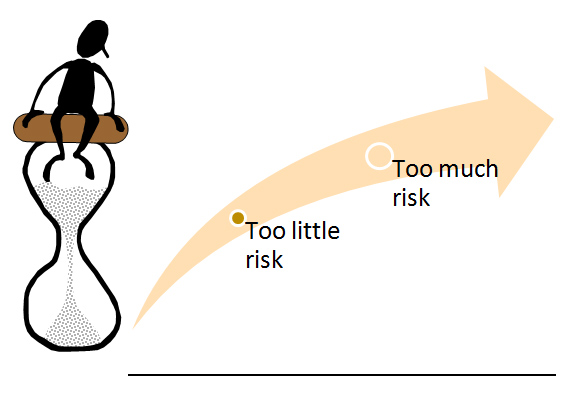

A common behavioral trait is Inertia – many times we find ourselves failing to act and doing nothing over a period of time as it pertains to our asset allocations. Our tendency to maintain our same level of exposure to equities and bonds year after year despite changes in our life circumstances and risk tolerances is the effect of inertia. Good investment practice will dictate a change in asset allocation as one ages and as one enters into new life chapters. For example, as a young investor, it is recommended that you have a large exposure to equities as there is enough time to recover from any dips in the stock market. As a retiree, you would arguably have less time to recover for any downturns in the stock market, hence it is recommended that your exposure to bonds increase and your investments in equities be reduced. By doing nothing, you will be exposing yourself to unnecessary risk – a risk that will be hard to recover from.

Figure 3: Portfolio impact on Inertia

Another pitfall many investors find themselves in is to employ a very simple diversification strategy – often called 1/n Naïve Diversification. This strategy sees the investor dividing their funds equally among available securities or investment vehicles, irrespective of the risk and return profile of the securities.While it may appear that the equal allocation strategy is sound, in reality it isn’t. By failing to recognize the differences as it pertains to the asset composition and risk and return characteristics of the various funds and securities, as an investor, you can assume too little risk or too much risk and run the chance of not achieving your financial goals.

Overconfidence is another key behavioral trait that many investors fall prey to. Overconfidence is a bias in which investors act upon unwarranted faith in their own intuitive reasoning and abilities. This behavior may stem from the tendency to overestimate one’s knowledge and experience and in the disillusioned belief that one is smarter and more informed than everyone else.

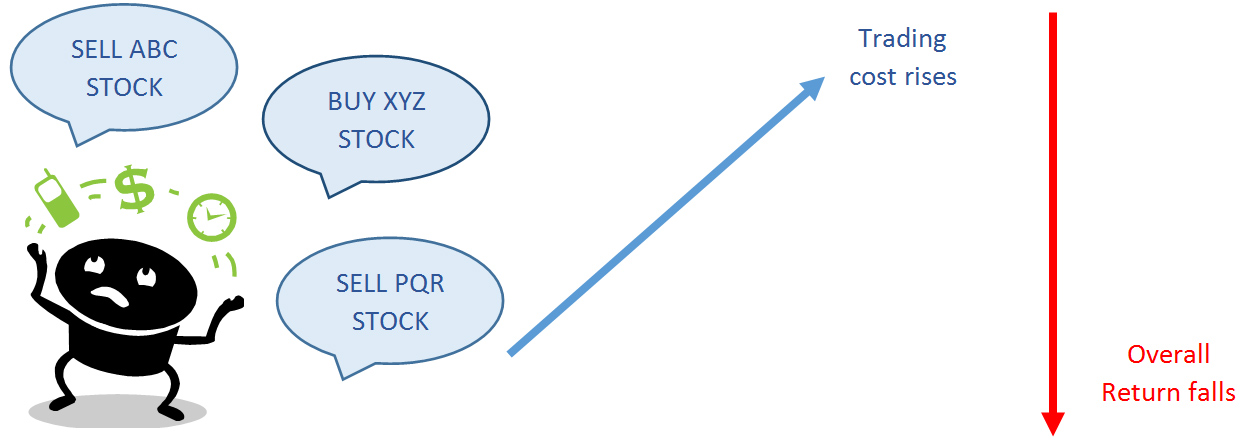

As an investor, overconfidence can lead you to trade excessively as there is the belief that you are better than the experts as it pertains to choosing stocks and in timing the stock market. Consequently, you may tend to buy and sell stocks frequently – such actions can erode whatever returns you may get. In order for any investor to buy or sell a share, the services of a broker must be sought after. It is very rare that investors can purchase shares directly from the stock market. The buying and selling of shares are normally achieved through the use of stock brokerage firms who are entities that conduct stock transactions on behalf of investors. This service is conducted for a fee or commission. With numerous trades, your commission and fees rise, thus reducing the overall return that you receive on your portfolio.

Figure 4: Trading cost and the impact on return

Anchoring is a common behavioral trait that many investors are susceptible to. As investors, investment opinions and ideas are generally based on information we are initially exposed to. Anchoring arises when we are faced with new information and fail to incorporate it into our decision making process – our initial opinion and ideas are “anchored” to the previous information or news. For example, we may have initially read the business performance of a particular company – this company had spectacular projects in the making that would have thrust them ahead of their peers.

Based on this information, we purchased the stock. Sometime later, news surrounding a critical deal that fell through for the company comes to our attention. The failure of this deal would directly impact the company’s plan to start their capital projects, making their strategic objective unattainable. This change of events causes the share price of the company to fall. Despite this knowledge, often than not, as investors, we tend to discount such negative information and any less favourable news and fail to take action – that is, sell or reduce our position in the particular stock.

Sometimes the behaviors of individual investors affects the stock market as a whole. There is the tendency for investors to follow blindly the investment action of others – such actions can lead to bubbles and crashes in the stock market. Mimicking the investment actions of others is called Herding and occurs when individual investors abandon their own private information and research and act as other investors do. There are many reasons why Herding behavior happens – one can be the social pressure for acceptance. Given the innate desire to be accepted, investors may opt to buy the stocks the masses are buying or selling in order to fit in and not be seen as an outcast.

Investors may also choose to follow the “pack” as it provides a false belief that a large group cannot be wrong. Investors may experience a certain degree of comfort and reassurance to be aligned with the masses and feel convinced that the masses may know something that they are not aware of. So following the old adage “better to be safe than sorry” investors jump right in and copy what other investors are doing.

As human beings, we cannot escape our emotions. As a consequence, more often than not, our decision making is affected by our emotions. As investors, our behavioral traits will play a part in deciding the type of securities we invest in, when we invest and how we react to gains and losses. We as investors tend to be overconfident in our own abilities and knowledge when selecting investments. We also tend to be anchored by our initial views and information and also follow what the masses are investing in.

In order to become a successful investor we should strive towards managing emotions. One way of overcoming this behavioral obstacle is to develop an investment plan that clearly outlines our return objectives and risk tolerance.The establishment of a detailed and comprehensive investment plan will help you to avoid making knee-jerk decisions to change your asset allocation when faced with passing trends in the stock market.

A Financial advisor at the Unit Trust Corporation can assist you in developing the right investment plan for you. Contact us at yourwealthmanager@ttutc.com or call 624-8648 extension 8113.

27TH June 2014 Sources • The Behavioural biases of Individuals, Michael M Pompian, CFA • Investopedia

You should consult with a Financial Advisor at the UTC, who can assist you in planning major life decisions and events.